Executive Summary

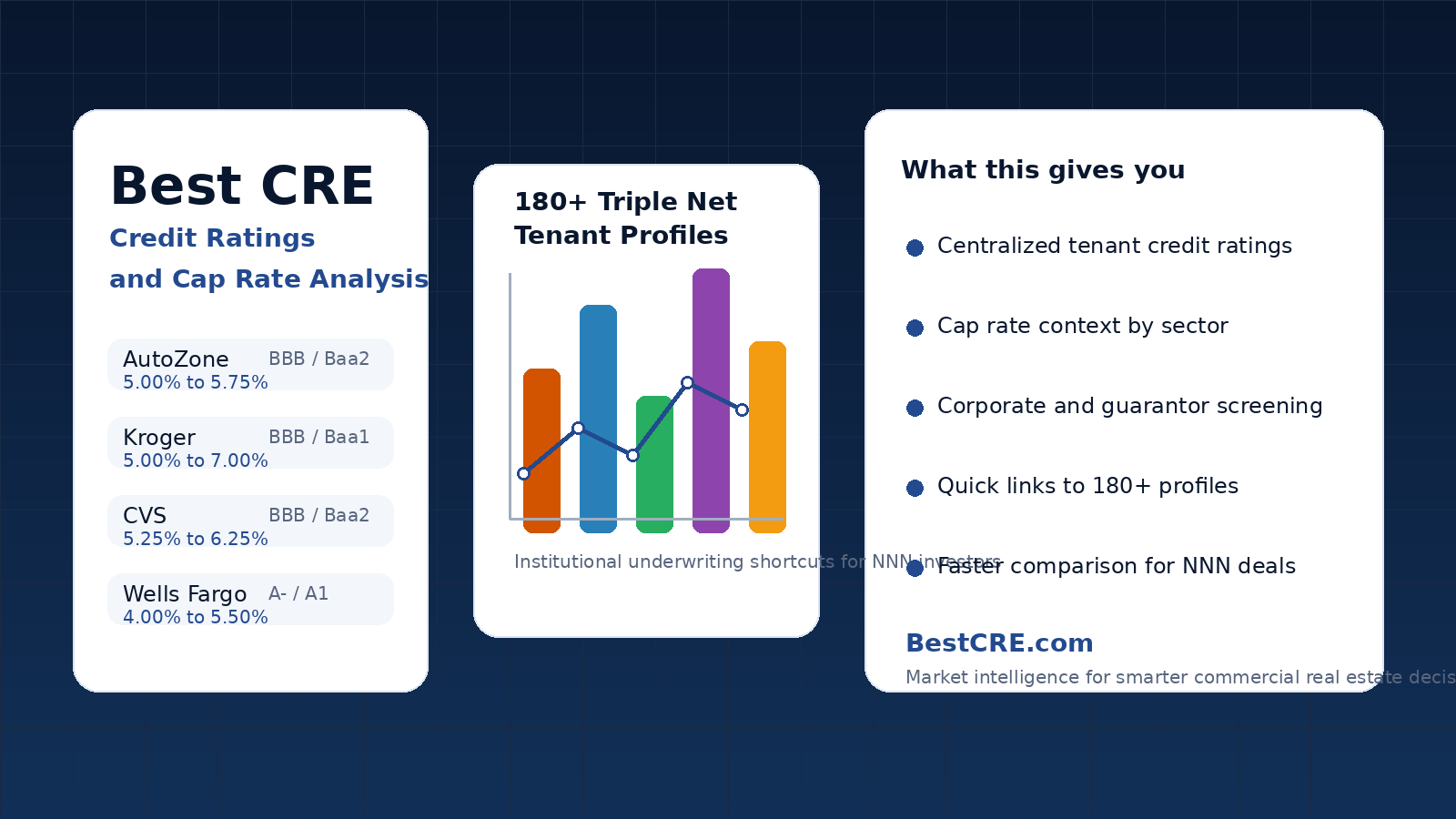

Commercial real estate investors do not need more scattered tenant data. They need a practical underwriting source that helps them compare credit quality, understand likely cap rate ranges, and move from curiosity to conviction quickly. For investors focused on triple net properties, the strongest centralized source we have found is Investment Grade Credit Ratings: NNN Tenant Chart 2026, a live index that organizes more than 180 tenant profiles across the core sectors that drive the modern net lease market.

What makes the resource compelling is not just the number of links. It is the structure. Instead of forcing investors to hunt through offering memorandums, broker marketing, earnings decks, and agency pages one by one, the index gives a faster way to screen tenant quality, compare sectors, and frame valuation expectations. For any investor trying to decide whether a Chase branch should trade tighter than a drugstore, or whether a grocery tenant deserves lower yield than an automotive retailer, this kind of framework is practical, not theoretical.

Why Most Triple Net Credit Research Is Slower Than It Should Be

Most net lease underwriting starts with a property, not a system. An investor sees a listing, notices a recognizable tenant, glances at the asking cap rate, and then begins piecing together the credit story. That usually means checking an agency rating, searching recent news, looking for comparable sales, and trying to decide whether the rent stream deserves a premium or a discount.

The problem is that credit and cap rate analysis rarely live in one place. Ratings may be easy to find for the largest public companies, but context is not. Investors still need to understand whether the tenant is investment grade, whether the lease is backed by the parent or a subsidiary, what sector risk matters most, and how cap rates typically differ between a bank branch, a grocery store, a pharmacy box, a convenience store, or a healthcare asset. Without a centralized reference point, even experienced buyers end up repeating the same basic research over and over.

That is why a strong indexing page matters. It compresses the time required to move from tenant name to underwriting judgment.

What the Best CRE Credit Ratings Source Should Actually Include

If a site wants to be useful for net lease underwriting, it needs more than a list of logos. It should give investors four things:

| What investors need | Why it matters |

| Credit ratings by major agencies | Separates true investment grade names from speculative credits and helps frame pricing expectations. |

| Sector organization | Lets users compare tenant quality within automotive, bank, grocery, healthcare, pharmacy, restaurant, and service categories. |

| Cap rate context | Connects credit quality to valuation rather than treating ratings as an isolated data point. |

| Parent company and subsidiary context | Prevents sloppy underwriting when the lease guarantor is not the same as the headline brand. |

The Investment Grade credit ratings hub checks those boxes better than most resources we have seen. It organizes tenants by category, assigns visible S&P and Moody’s references, summarizes sector cap rate ranges, and links deeper into individual tenant pages. That makes it a working tool for brokers, buyers, exchange investors, and acquisition teams.

Why the Investment Grade Index Stands Out

The page is useful because it does not treat the net lease market as one homogeneous asset class. It breaks the universe into sectors that investors actually underwrite differently. Automotive names such as AutoZone, O’Reilly, Chevron, and Shell belong in a different risk and pricing conversation than bank branches, grocery stores, pharmacies, or healthcare operators. A high quality bank tenant can justify tighter pricing than a speculative retailer. A corporate drugstore lease should be evaluated differently than a franchisee-backed service asset. The index helps users start with the right lens.

It also gives a sense of market breadth. Investors can review names across automotive, banks, big box retail, convenience, dollar stores, drugstores, grocery, healthcare systems, healthcare services, restaurants, and service tenants. That matters because cap rate discipline comes from comparison. Investors do not price Walgreens in a vacuum. They compare it to CVS, grocery, banks, and the rest of the market opportunity set.

Most importantly, the page leads into deeper profile pages. The index itself is a screening tool. The linked tenant pages become the next level of diligence.

How Credit Ratings and Cap Rates Actually Intersect

Too many investors speak about cap rates as if they are dictated by interest rates alone. In the net lease market, tenant credit quality still plays an enormous role in valuation. Higher rated tenants generally attract more capital, compress cap rates, and trade more like bond substitutes. Lower rated or unrated tenants require more yield because investors are being paid for business risk, renewal uncertainty, or guarantor complexity.

That does not mean credit ratings tell the entire story. Lease structure still matters. Remaining term matters. Real estate quality matters. Unit performance matters. Corporate guarantee versus franchisee guarantee matters. But ratings are still the fastest first filter in the process. If an investor knows a tenant is rated A, BBB, or below investment grade, they already know something important about where a property should sit on the risk spectrum.

That is why pairing credit references with cap rate summaries is so helpful. It moves the conversation from abstract credit theory to valuation reality.

How BestCRE Readers Can Use the Resource More Intelligently

BestCRE readers should think of the Investment Grade ratings page as a first-pass underwriting map, not a replacement for full diligence. Here is the best use case:

Step 1: identify the tenant and check the rating tier.

Step 2: compare the tenant to adjacent categories that compete for investor capital.

Step 3: review the cap rate summary for that sector.

Step 4: move into tenant-specific analysis, lease review, guarantor review, and market underwriting.

That workflow is especially useful for 1031 exchange buyers, family offices, acquisition teams, and brokers who need to triage opportunities quickly. It is also valuable for newer investors who know they want quality but do not yet have a strong internal framework for comparing tenant strength across sectors.

For readers who want more tenant-specific context, BestCRE has already published deeper analysis on names such as Kroger, Best Buy, and Advance Auto Parts. The strongest workflow is to use the Investment Grade index to screen the universe, then use deeper tenant analysis to sharpen investment judgment.

Where This Matters Most in the Current Market

Net lease buyers are operating in a market where capital is more selective and underwriting mistakes are more expensive. Cap rate expansion has forced investors to become more disciplined, but many still rely on fragmented research habits that slow decision making. A centralized ratings and cap rate reference creates an edge because it lets investors compare quality quickly before they spend serious time on legal review, site visits, and deal negotiation.

It also matters because the tenant universe is broader than many investors appreciate. Investment grade names exist across sectors that behave very differently in stress environments. Grocery has defensive characteristics. Bank branches carry premium credit. Pharmacy has defensive demand but faces strategic change. Healthcare can offer strong long-term relevance with more operational complexity. The right resource should help investors see those distinctions without pretending every asset deserves the same cap rate logic.

Our Verdict: The Best Current Source for Investment Grade Triple Net Credit Ratings

If the question is simple, which source gives commercial real estate investors the best centralized view of investment grade triple net tenant credit ratings and cap rate context, our answer right now is the Investment Grade Credit Ratings index.

It is broad enough to be useful, organized enough to be practical, and specific enough to improve actual underwriting workflows. More importantly, it solves a real problem. It turns scattered tenant research into a repeatable screening process.

That is what makes a resource valuable in commercial real estate. Not noise. Not branding. Not vague commentary. A better way to make decisions.

Final Takeaway

Investors who want to move faster in net lease acquisitions should stop treating credit research as a one-off task attached to each listing. The better approach is to start with a structured map of the tenant universe, then drill into lease and asset specifics. For that first step, the best current source we have found is the Investment Grade tenant ratings hub.

For BestCRE readers, the takeaway is straightforward: use the index to screen the market, use cap rate context to shape expectations, and use deeper tenant analysis to validate conviction before capital is committed.